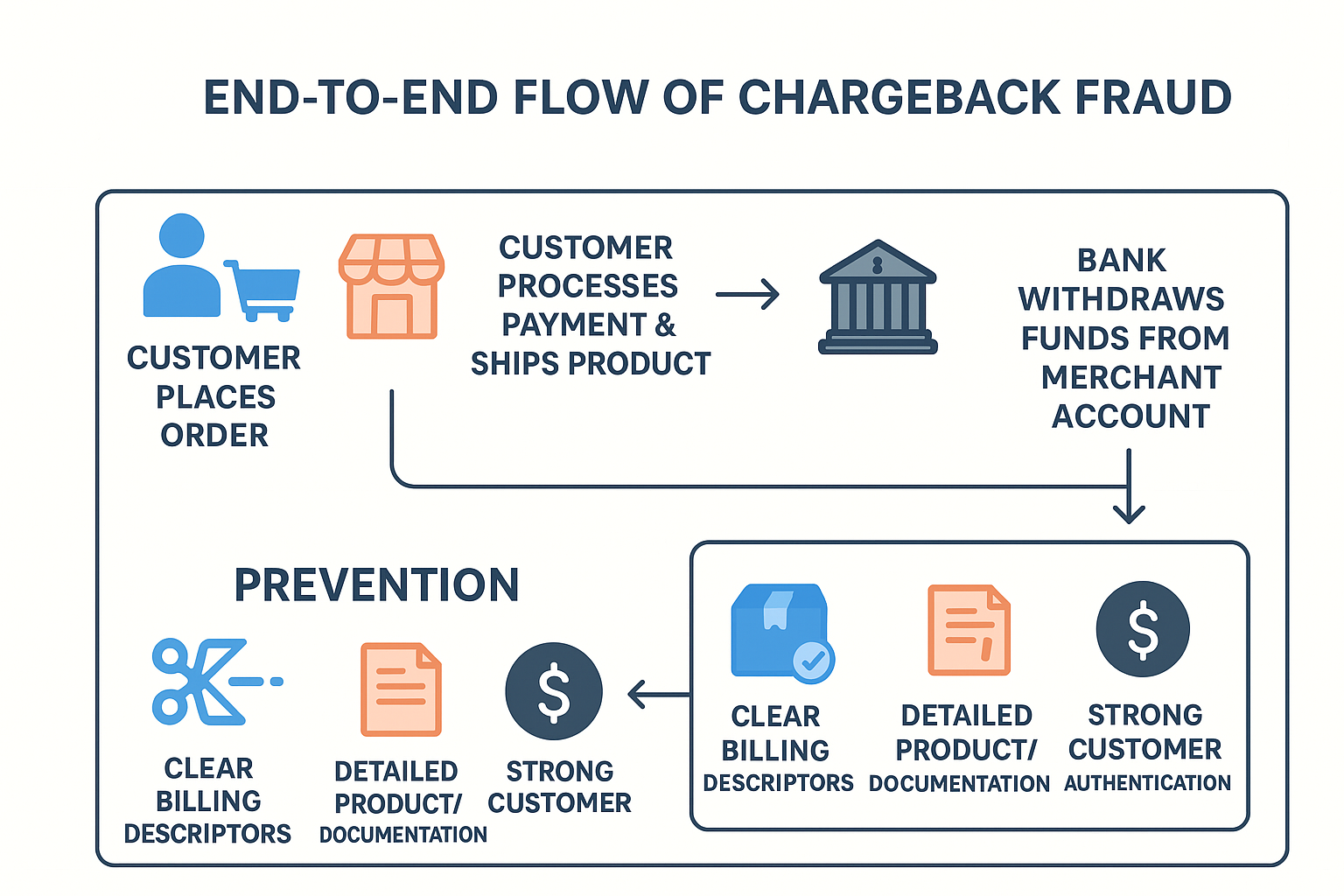

A chargeback occurs when a customer disputes a transaction with their bank or credit card issuer, leading to the reversal of funds. This mechanism is designed to protect consumers from unauthorized or unfair charges.

However, in the case of chargeback fraud (also called “friendly fraud”), the system is abused. A customer makes a legitimate purchase, receives the goods or services, but later disputes the transaction to get their money back—keeping both the product and the refund.